You don’t have to wait until you’re ready to sell your house to gain access to your home equity — using that money to pay for your current needs or goals could be a smart play.

If you’re a homeowner, you have probably heard the term “home equity” often, and you may have a general understanding of how homeownership builds wealth over time.

But, if you own a home, now could be a perfect time to take a closer look at your unique home equity and how it could benefit you now.

What is Equity?

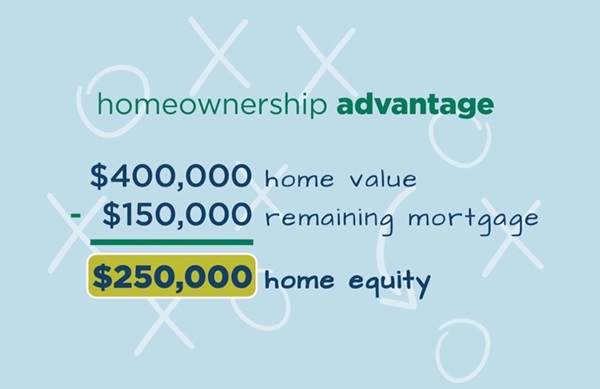

Long story short: your home equity is the difference between how much your home is worth and how much you still owe on the mortgage.

For example, if you own a house that’s worth $400,000, and you still owe $150,000 on the mortgage, your home equity is roughly $250,000.

What Can I Do with My Home Equity?

Most people don’t think about their home equity until they are ready to sell their house. But what if you could tap into your equity to help pay for some of the needs or dreams that you have right now?

There are several different ways you can use your home equity to achieve personal goals, pay down debt, or make home renovations.

After all, life is happening now. Why not use one of your greatest assets — your home — to support your current goals?

Your home equity can be used for a variety of purposes. Here are some of the common ones…

- Home Improvements: These can include kitchen remodels, bathroom renovations, adding a room, or making energy-efficient improvements.

- Home Repairs: If your home requires urgent repairs, such as a new roof or foundation repairs, tapping into your home equity can be a practical way to cover these costs.

- Debt Consolidation: You can use your home equity to combine high-interest debt like credit card balances or personal loans. By doing this, you may lower your overall interest rate and streamline your monthly payments.

- Education Expenses: Home equity can help pay for education costs, such as tuition, books, and school-related expenses. This can be a cost-effective way to finance education compared to other borrowing options.

- Emergency Expenses: You can use your home equity to pay unexpected medical bills or other financial emergency expenses at a lower interest rate than credit cards or personal loans.

How Can I Access My Home Equity?

In general, there are four common ways you can access your home equity…

Home Equity Loan

Known as a “second mortgage,” a home equity loan allows homeowners to borrow a lump sum of money based on their equity. This type of loan, also called a HELOAN, usually has a fixed interest rate and is repaid in regular installments over a specific timeframe.

Home Equity Line of Credit (HELOC)

With a HELOC, you receive a credit limit based on your home’s equity, which you can draw from as needed. Unlike a home equity loan, a HELOC typically has a variable interest rate. At Waterstone Mortgage, we offer a fixed-rate* HELOC option, which allows you to access all funds at closing, then make additional draws throughout the draw period.

Cash-Out Refinance

A cash-out refinance involves taking out a mortgage greater than the remaining balance on your current loan, using your equity as a cash advance. With this option, you refinance your original mortgage loan into a new loan.

Reverse Mortgage

A reverse mortgage is a loan for homeowners ages 62+ that does not have to be paid back for as long as the homeowner lives there. In general, a reverse mortgage is most beneficial to homeowners who are still paying a conventional mortgage but would rather free up that money to use for other expenses (such as medical bills, utilities, home repairs, or renovations) or to build up their savings.

Home Equity Strategies

So, now that you understand the methods you can use to tap into your home equity, let’s look at some possible plays you might make, depending on your situation…

To give you an idea of how you can effectively use your home equity, we put together a list of what we like to call our Homeownership Advantage scenarios — a “playbook,” if you will — that will inspire you to get creative when tapping into your strongest asset: your home equity.

Playbook Strategy #1: Home Equity Loan for Renovations

The Scenario: You’re going on year #8 in your starter house. It’s been an awesome home, but you’ve added two children to your family in recent years and had hoped to upgrade to a larger space by now. But, moving to a new home isn’t currently on your radar.

The Play: By taking out a home equity loan (essentially, a second mortgage), you can access your home equity to renovate the basement — adding the extra living space you need right now.

The benefit of a home equity loan is that it typically has a lower interest rate than personal loans or credit cards. So, if you don’t have cash to pay for your home renovations, a home equity loan could save you money in comparison to other high-interest debt you would otherwise have to resort to.

Another advantage of home equity loans is that you can deduct the interest paid on your loan annually on your tax return (although, specific conditions apply — ask your loan originator for details).

Plus, when you eventually decide to sell your home, your home renovations will add value — and will likely give you a greater return on your investment. In this way, a home equity loan could end up saving you money, if you’re able to list your home for a higher price and receive higher offers.

Playbook Strategy #2: Cash-Out Refinance to Eliminate Credit Card Debt

The Scenario: You are generally responsible with your finances, but you went through a difficult time when you charged most of your expenses to credit cards — culminating in more debt than you had planned to take on. Now, you have high-interest credit card debt totaling $20,000, and the monthly payments are taking a toll on your finances and credit score.

The Play: Using a cash-out refinance, you can access your home equity and receive a lump sum of cash to pay off your credit card debt.

Let’s say your home is worth $400,000 and you still owe $150,000 on the mortgage. You need $20,000 to pay off your credit cards, so you do a cash-out refinance and take on a new mortgage:

While your new mortgage is higher than your previous one, this cost-effective strategy allows you to pay off your credit card debts, which cumulatively would have cost you much more in interest over the years.

Now, free of credit card debt, you can focus your efforts on maintaining healthy finances for the future.

Playbook Strategy #3: HELOC to Pay for College

The Scenario: You’re considering going back to college to finish the degree you’ve always dreamed of earning — but the thought of taking out student loans makes you hesitant.

The Play: As a homeowner, you can take out a Home Equity Line of Credit (HELOC) to cover tuition payments. Because HELOCs typically have lower interest rates than private student loans, this could save you a significant chunk of money over time.

Usually, HELOCs allow you to borrow up to 90% of the equity in your home. So, let’s say your home is valued at $300,000 and you have $200,000 remaining on the mortgage. Your equity is $100,000.

So, if you can borrow up to 90% of your home equity, you could potentially receive a line of credit up to $90,000 to use toward your college expenses:

It works like a credit card, because you can access your funds (up to the limit) at any time during the draw period.

This may also save you money because you can take the money out on an “as-needed” basis — instead of receiving one lump sum. So, if tuition costs fluctuate and end up being less than you expected for certain semesters, you could save money by not accruing interest on funds you haven’t yet borrowed.

Playbook Strategy #4: Reverse Mortgage to Pay for Increasing Expenses

The Scenario: You’re a senior homeowner (age 62+) who is experiencing increasing costs, such as homeowners insurance, medical bills, and food expenses.

The Play: Using a reverse mortgage, you can tap into your home equity and receive a lump sum of cash to pay off credit cards and medical bills, and to eliminate your monthly mortgage payment and free up cash flow for other expenses.

A reverse mortgage allows an eligible homeowner (ages 62+) to receive proceeds in the form of a lump sum, a regular monthly payment, or a line of credit (or any combination of those three).

Now, with your expenses under control, you can enjoy the next phase of life in your house — which you plan to stay in for many years to come.

What’s Your Next Play?

These are just a few of the ways you could tap into your home equity to achieve your goals and address your financial needs. You don’t have to sit on the sidelines, waiting to access your home equity — you can use that wealth now! All it takes is a quick, complimentary conversation with a trusted loan originator to determine your best options.

*The initial amount funded at origination will be based on a fixed rate; however, this product contains an additional draw feature If the customer elects to make an additional draw, the interest rate for that draw will be set as of the date of the draw and will be based on an Index, which is the prime rate published in the Wall Street Journal for the calendar month preceding the date of the additional draw, plus a fixed margin. Accordingly, the fixed rate for any additional draw may be higher than the fixed rate for the initial draw.

Geographical restrictions apply, contact your mortgage loan professional for additional information. Some programs may be available through a broker relationship with other lenders. Waterstone Mortgage is not affiliated with those lenders. Credit approval is at the sole discretion of the lender. Consult a tax advisor for questions about tax and government benefit implications.

These materials are not from HUD or FHA and were not approved by HUD or a government agency. The only reverse mortgage insured by the U.S. Federal Government is called a Home Equity Conversion Mortgage (HECM), and is only available through a Federal Housing Administration (FHA)-approved lender. Not all reverse mortgages are FHA insured. When the loan is due and payable, some or all of the equity in the property that is the subject of the reverse mortgage no longer belongs to borrowers, who may need to sell the home or otherwise repay the loan with interest from other proceeds. A lender may charge an origination fee, mortgage insurance premium, closing costs and servicing fees (added to the balance of the loan). The balance of the loan grows over time and you are charged interest on the balance. Borrowers are responsible for paying property taxes, homeowner’s insurance, maintenance, and related taxes (which may be substantial). There is no escrow account for disbursements of these payments. A set-aside account can be set up to pay taxes and insurance and may be required in some cases. Borrowers must occupy home as their primary residence and pay for ongoing maintenance; otherwise the loan becomes due and payable. The loan also becomes due and payable (and the property may be subject to a tax lien, other encumbrance, or foreclosure) when the last borrower, or eligible non-borrowing surviving spouse, dies, sells the home, permanently moves out, defaults on taxes, insurance payments, or maintenance, or does not otherwise comply with the loan terms. Interest is not tax-deductible until the loan is partially or fully repaid.

Refinance requests are subject to credit approval as well as specific loan program requirements and guidelines. A Waterstone Mortgage professional can answer your questions and assist you in the application process should you choose to proceed.